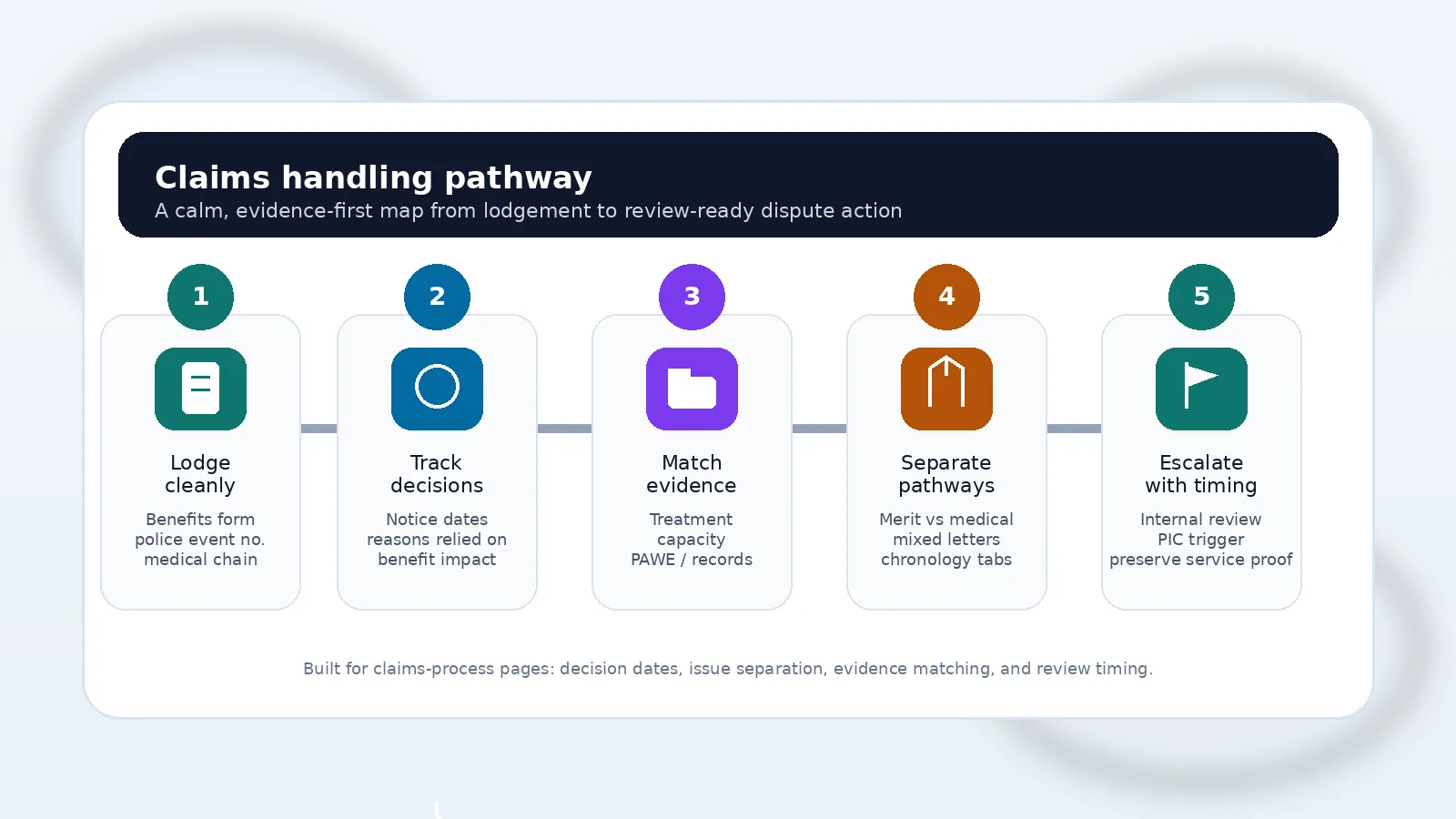

NSW CTP claims process (Guidelines Part 4 — overview)

Part 4 of the SIRA Motor Accident Guidelines deals with claims handling. This page provides a plain-English overview of the typical claim stages and the claims-handling expectations that often sit behind insurer decision-making. General information only.

Quick answer

Part 4 of the SIRA Motor Accident Guidelines deals with claims handling. This page provides a plain-English overview of the typical claim stages and the claims-handling expectations that often sit behind insurer decision-making. General information only.

Why this guide is structured this way

This page is written to help NSW CTP claimants understand deadlines, evidence, insurer decisions, and dispute pathways in plain language without overstating outcomes.

General information only. Your position depends on your facts, evidence, insurer response, and applicable time limits.

Top questions answered

Does Part 4 apply to every claim?

Part 4 broadly concerns claims handling in the NSW scheme. Transitional provisions can apply depending on accident date and the clause in question.

What should I do if the insurer makes a decision I disagree with?

Get the decision in writing, identify the reason and evidence relied on, and consider internal review and the PIC pathway depending on the decision type.

Do I need a lawyer for the claims process?

You can lodge a claim without a lawyer, but disputes about threshold injury, WPI, capacity, and treatment can be technical. Advice can help with evidence and deadlines.

Starting the claim

Most claims begin with lodging the correct benefits application and providing initial supporting material. Early medical records and accurate accident reporting often become key evidence later.

Read: How to lodge a NSW CTP claim.

Insurer decision points

Insurers make multiple decisions over time, for example about liability, weekly payments, treatment approvals, threshold injury classification, and (in some matters) permanent impairment/WPI issues.

Common dispute triggers include weekly payments stopped and treatment refused.

Evidence and communication

Claims handling is evidence-driven. Good outcomes usually depend on targeted evidence that addresses the insurer’s stated reasons and the relevant legal tests (for example threshold injury definition, work capacity, causation, and reasonable and necessary treatment).

Where the insurer says you can return to work or reduces benefits based on earning capacity, it helps to separate the medical evidence from the weekly-payments and earnings issues. See capacity for work disputes and PAWE calculation.

Disputes, internal review and PIC

Many disputes start with internal review and then (if unresolved) escalate to the PIC in the correct dispute category.

Read: Internal review, Dispute resolution guidelines, and Merit vs medical assessment.

What usually makes a stronger claims-handling challenge

Where a claimant says the insurer has mishandled the claim, the stronger file usually does more than complain about delay or unfairness in general terms. It identifies the exact decision, the date it was made, the guideline topic engaged, and the practical effect on benefits, treatment, work capacity, or settlement position.

Useful evidence often includes the decision notice, certificates, treating recommendations, wage records, rehabilitation correspondence, and a short chronology showing what was requested, when it was sent, and what the insurer did or failed to do next. That approach usually works better than sending a large bundle with no explanation of why each document matters.

If the problem centres on stopped benefits, capacity, treatment, or settlement conduct, it helps to cross-check the file against weekly payments stopped, capacity for work disputes, treatment refused, and PIC settlement approval.

Common mistakes when relying on the claims process guidelines

One common mistake is treating every insurer problem as the same kind of dispute. Claims handling, treatment, earnings, threshold injury, and WPI issues can overlap, but they do not always travel through the same review path or need the same evidence.

Another frequent problem is waiting too long to preserve the paper trail. If an insurer delays, changes position, or says information was never provided, it helps to keep copies of requests, certificates, treatment plans, wage documents, and acknowledgment emails or website/claim-system messages.

A third mistake is focusing only on broad fairness arguments instead of the actual legal and guideline issue. In practice, a sharper submission usually maps each complaint back to the decision, the missing evidence, the review step, and the next escalation option if the insurer does not fix the issue.

When a claims-process problem becomes review-ready

Not every frustration with an insurer is immediately ready for internal review or PIC escalation. Usually, the file becomes review-ready when there is a clear decision, delay, refusal, reduction, or failure to act that can be tied to a specific benefit, treatment request, work-capacity position, or settlement step.

That usually means preserving the trigger document itself, confirming dates, and showing the practical consequence on the claim. If the insurer is delaying while weekly payments stop, treatment remains on hold, or an earning-capacity position is affecting entitlements, it helps to move quickly and organise the file around internal review, weekly payments stopped, capacity disputes, and treatment disputes.

Where the real issue is delay, poor reasons, or mixed pathway handling, a concise chronology often matters as much as the medical material. It helps show the decision-maker what happened, what was provided, what was ignored, and why the problem is no longer just administrative inconvenience but a live entitlement dispute.

When claims-process issues overlap with guideline and PIC stream selection

Many live claims-process disputes are not really just about delay. They often involve a second issue hiding underneath, such as a treatment refusal, a work-capacity dispute, a PAWE calculation disagreement, or a threshold/WPI classification problem that has not yet been framed properly.

That matters because the claims-process complaint may explain how the insurer handled the file, but the remedy often depends on identifying what the substantive dispute actually is. If the insurer has mixed medical and merit issues together, claimants usually do better by separating the streams early and cross-checking the broader Motor Accident Guidelines, dispute resolution guidance, merit review vs medical assessment, and PIC pathways.

For that reason, a good claims-process file often becomes stronger once the user can say not only that the insurer handled the matter badly, but also whether the underlying fight is really about treatment, weekly benefits, work capacity, threshold injury, permanent impairment, or settlement timing.

When claims handling problems affect settlement decisions

Claims-process issues can become especially important once a matter moves toward negotiation or settlement. A claimant may feel pressure to accept an offer because weekly payments have stopped, treatment has been delayed, or the insurer has kept the file in a state of uncertainty for months. In those situations, the claims-handling problem is no longer just administrative; it can directly distort settlement behaviour.

That is one reason it helps to test settlement readiness separately from insurer pressure. Before resolving the matter, it is usually worth checking whether treatment disputes are still active, whether capacity or PAWE issues remain unresolved, whether threshold or WPI questions are still developing, and whether the file is mature enough for a fair damages assessment. Useful cross-check pages include settlement process, non-economic loss, weekly payments stopped, and PIC settlement approval.

From a user-experience perspective, the practical question is often not just whether the insurer has been difficult, but whether the claims handling has pushed the claimant toward a premature outcome. Framing the issue that way usually produces a better evidence plan and a safer next-step decision.

Records that usually matter most when claims handling breaks down

When a claimant later says the insurer failed to act properly, the most useful records are usually the boring ones people forget to keep: acknowledgment emails, certificate chains, treatment requests, rehab correspondence, wage records, notices of decision, and any message showing what the insurer asked for and when it was provided.

Those records matter because they let the claimant prove sequence, not just frustration. They can show that a certificate was current when benefits were reduced, that treatment support existed before it was refused, or that the insurer was given the material it later said was missing. In many review matters, chronology wins more ground than rhetoric.

For live disputes, it often helps to organise those records into small issue-specific bundles connected to internal review, capacity disputes, PAWE issues, treatment refusals, and PIC stream selection rather than keeping one large undifferentiated claim file.

How to handle insurer notices that mix several issues together

One of the more confusing claims-process problems is the insurer letter that appears to decide several different things at once. A single notice might discuss treatment, work capacity, weekly benefits, and threshold language in the same document. When that happens, claimants often lose time because they answer the letter as if it contains only one dispute.

A safer approach is to break the notice into issue-specific parts: what is being said about treatment, what is being said about earnings or capacity, what is being said about medical classification, and what review path each point is likely to follow. That usually makes the response clearer and reduces the risk of sending strong evidence to the wrong stream.

In practice, mixed notices are often easier to handle when the response bundle is grouped into separate tabs or mini-sections linked to treatment disputes, weekly payments stopped, capacity disputes, threshold classification issues, and PIC merit vs medical stream selection. That kind of organisation helps both users and decision-makers see that the claim is not just messy; it contains several distinct questions that need to be answered properly.

When poor insurer communication becomes part of the dispute

Another recurring claims-process problem is the insurer who does not clearly explain what is missing, why a decision has been made, or what the claimant needs to provide next. Sometimes the file drifts because the claimant is told only in broad terms that more information is needed, without a usable explanation of whether the real issue is treatment support, work capacity, PAWE, threshold injury, or simple chronology gaps.

When communication breaks down, it usually helps to answer in a structured way rather than sending more unsorted material. A short response that identifies the disputed issue, lists what has already been provided, states what remains unclear, and asks the insurer to confirm the exact decision pathway often creates a much cleaner record for later internal review. This is especially useful where the claim overlaps with stopped weekly payments, treatment refusal, PAWE, or threshold injury classification.

From a dispute-readiness perspective, poor communication matters because it can show that the issue is not just lack of evidence but lack of decision clarity. If a claimant later needs internal review or a PIC application, a clean paper trail showing unclear reasons, moving requests, or unexplained delay can materially strengthen the chronology and help frame the real dispute earlier.

Build a decision map before you challenge the insurer

One of the most useful claims-process habits is building a simple decision map before sending any review material. That means listing each insurer notice, the date, the issue being decided, the evidence relied on, the missing evidence complained about, and the review or escalation path that may apply next.

This matters because many claimants respond to the latest insurer letter as if it exists in isolation. In reality, the better file usually shows how one decision triggered the next: a delayed certificate led to a work-capacity argument, that argument affected weekly payments, the weekly-payments decision put treatment at risk, and the resulting pressure distorted settlement discussions. Mapping the chain helps separate symptoms of poor claims handling from the real dispute stream underneath.

For practical routing, a decision map often works best when it points outward to the next exact page or process, such as benefits lodgement, medical certificate requirements, weekly payments stopped, capacity disputes, and PIC stream selection instead of treating the whole file as one vague fairness complaint.

Distinguish delay problems from substantive entitlement problems

Another high-value distinction is whether the real complaint is delay itself or whether delay is simply the way a substantive dispute is showing up. If an insurer is taking too long to answer but the underlying fight is really about treatment reasonableness, earning capacity, threshold classification, or insurer identity, the claimant usually gets a better result by preparing for that substantive dispute early rather than arguing only about speed.

That does not mean delay is irrelevant. Delay can be extremely important where it causes a missed surgery window, forces a gap in weekly benefits, interrupts rehabilitation, or pressures the claimant into a premature settlement position. But even then, the stronger challenge usually explains both the process failure and the entitlement consequence created by it.

In practice, this often means preserving two connected records: a chronology showing the delay, and an issue-specific bundle showing why the delayed decision mattered. That dual approach tends to be more useful for internal review, PIC dispute resolution guidance, and later settlement approval questions than a general complaint that the insurer was hard to deal with.

Practical checklist before internal review or PIC filing

Before escalating a claims-process problem, it usually helps to run a short checklist: do you have the decision notice, the current certificate chain, the key treating support, the wage or PAWE records if earnings are affected, and a dated chronology showing what was requested and when? If one of those elements is missing, the next step may be evidence repair rather than immediate escalation.

It also helps to ask whether the dispute bundle is too mixed. Review bodies usually find it easier to follow a file where treatment, benefits, capacity, threshold, and settlement issues are separated into clean sub-bundles with short explanations. That is often safer than attaching a large claim archive and expecting the decision-maker to reconstruct the dispute for you.

Where the answer to that checklist is yes, the matter is usually in a much better position for internal review process, PIC filing, guideline cross-checking, and specialist support if the claim has become too technical to manage alone.

If insurer identity is unclear: keep the claim moving while you investigate

Claims-process friction is common where insurer identity is uncertain (for example no rego, incomplete details, interstate complications, or conflicting crash information). The practical mistake is waiting passively for certainty while evidence gets older and deadlines tighten.

A safer approach is to run two tracks at once: preserve time-sensitive evidence immediately (police event details, witness contacts, photos, treatment chronology, and wage impact documents), and in parallel work through insurer-identification or Nominal Defendant pathways. That keeps the file active and reduces avoidable delay arguments later.

Useful pathways are identifying the correct insurer, Nominal Defendant, and lodging without rego details. If those issues are mixed with treatment or weekly-payment disputes, separate each stream early so procedural uncertainty does not swallow substantive entitlement issues.

Before you send your response: name the exact decision you want changed

Many otherwise strong claim files fail at a basic step: they do not clearly state which insurer decision is being challenged and what outcome is sought. If your letter says only that the process was unfair, the reviewer may agree in principle but still leave the decision untouched.

Before sending anything, write one plain sentence at the top of your submission: the decision date, the issue (for example treatment refusal, work capacity, PAWE, threshold, or mixed notice), and the correction you are asking for. That single sentence often improves review outcomes because it gives the decision-maker a precise target.

Then structure the rest of the submission to match that target: evidence first, chronology second, and pathway request third. If the file is still mixed, split it into short issue tabs linked to internal review, PIC stream selection, and the relevant dispute guides.

Frequently asked questions

- Does Part 4 apply to every claim?

- Part 4 broadly concerns claims handling in the NSW scheme. Transitional provisions can apply depending on accident date and the clause in question.

- What should I do if the insurer makes a decision I disagree with?

- Get the decision in writing, identify the reason and evidence relied on, and consider internal review and the PIC pathway depending on the decision type.

- Do I need a lawyer for the claims process?

- You can lodge a claim without a lawyer, but disputes about threshold injury, WPI, capacity, and treatment can be technical. Advice can help with evidence and deadlines.

- Where does the PIC fit?

- The PIC determines many disputes after internal review, using the correct dispute pathway.

- What if I do not have the other vehicle’s rego?

- There may still be options, including Nominal Defendant pathways in some circumstances. Evidence can be time-sensitive.

- If the insurer says I used the wrong pathway, does that end my claim rights?

- Usually no. A pathway dispute does not automatically extinguish treatment, weekly payment, or dispute rights. Ask for written reasons, separate each issue (treatment, capacity, PAWE, threshold), and preserve a dated evidence trail so internal review or PIC can assess each question properly.

- Can one mixed insurer letter be challenged in a single response?

- It can, but one blended response is often weaker. In practice, outcomes are usually better when you split the letter into issue-specific parts (for example treatment, capacity, PAWE, threshold), attach evidence to each part, and make a clear request for each pathway.

- The insurer says no further review can happen until a new specialist report arrives. Is that always correct?

- Not always. Insurers should still explain their current position on the evidence already available. If a further report is genuinely needed, ask them to identify exactly what issue it is meant to resolve, preserve a dated chronology of requests and responses, and keep progressing any dispute stream that is already review-ready rather than letting the whole claim stall.

- The insurer relies on one short surveillance clip to say I am recovered. Is that enough?

- Usually not by itself. A single clip can show a moment, but not your sustained function over days or weeks. Respond with a dated timeline that covers post-activity pain flare, sleep disruption, medication changes, and next-day limits, then ask the insurer to explain why that broader clinical record does not outweigh the isolated footage.

- The insurer asks me to sign a broad authority for “all records”. Should I just sign everything?

- Be careful with blanket authorities. It is usually safer to ask what date range and issue the request relates to, then provide targeted records relevant to the live dispute. Over-broad releases can create delay and noise, especially where the real issue is treatment approval, capacity, PAWE, threshold, or WPI.

- What is the fastest way to make my review request easier to decide?

- Start with a one-line decision target: identify the insurer decision date, the exact issue being challenged, and the correction sought. Then attach only evidence that answers that issue directly, followed by a short chronology. Review outcomes are usually better when the request is precise, not just comprehensive.

- When should I use specialist referrals instead of a general contact enquiry?

- If your matter already involves mixed issues (for example treatment plus work-capacity plus PAWE, or a review/PIC deadline running), specialist referral intake is usually safer because it routes the file with issue-specific context from the start. General contact can still be fine for early orientation, but once pathways and timing are in play, structured referral triage usually reduces avoidable delay.